✈️ Final Approach: 6 Smart Tax Moves Pilots Should Make Before April 15th

Tax season hits like a surprise holding pattern—and if you’re like most pilots, it probably wasn’t at the top of your to-do list. Between bidding schedules, simulator sessions, and layovers, it’s easy to push paperwork aside.

But with the April 15th deadline on final approach, there’s still time to take a few critical steps that could save you money, reduce stress, and even set you up better for next year.

Here are six things you can do today to get your taxes on glidepath:

1. Gather All Income Sources

Pilots often wear more than one hat—flying trips, instructing on the side, renting out property, or investing.

✅ Action Item: Make sure you’ve collected all your income documents:

-

W-2 from your airline

-

1099s from side hustles (e.g. flight instruction, Airbnb)

-

Investment income (1099-INT, 1099-DIV, etc.)

-

Rental property income and expenses

Don’t forget per diem reimbursements—these can be deductible depending on your employment structure and how much was pa...

Navigating Financial Skies with Budgeting

As commercial airline pilots, managing personal finances effectively is essential amidst the dynamic nature of our careers.

To navigate the financial skies with confidence, it's crucial to employ the right budgeting strategies. Here are five tailored budgeting approaches to help pilots take control of their finances and soar towards their financial goals.

- Traditional Budgeting:

- Track income and expenses meticulously, either manually or using user-friendly budgeting apps.

- Categorize expenses to gain insights into spending patterns, such as housing, travel, and aviation-related costs.

- Identify areas for optimization to ensure financial stability amidst fluctuating income and expenses.

- 50/30/20 Rule:

- Allocate 50% of income to essential needs like housing, utilities, and aviation-related expenses.

- Dedicate 30% to discretionary spending, including travel adventures, hobbies, and relaxation.

- Commit 20% to savings and investments, ensuring a solid financial foundation f ...

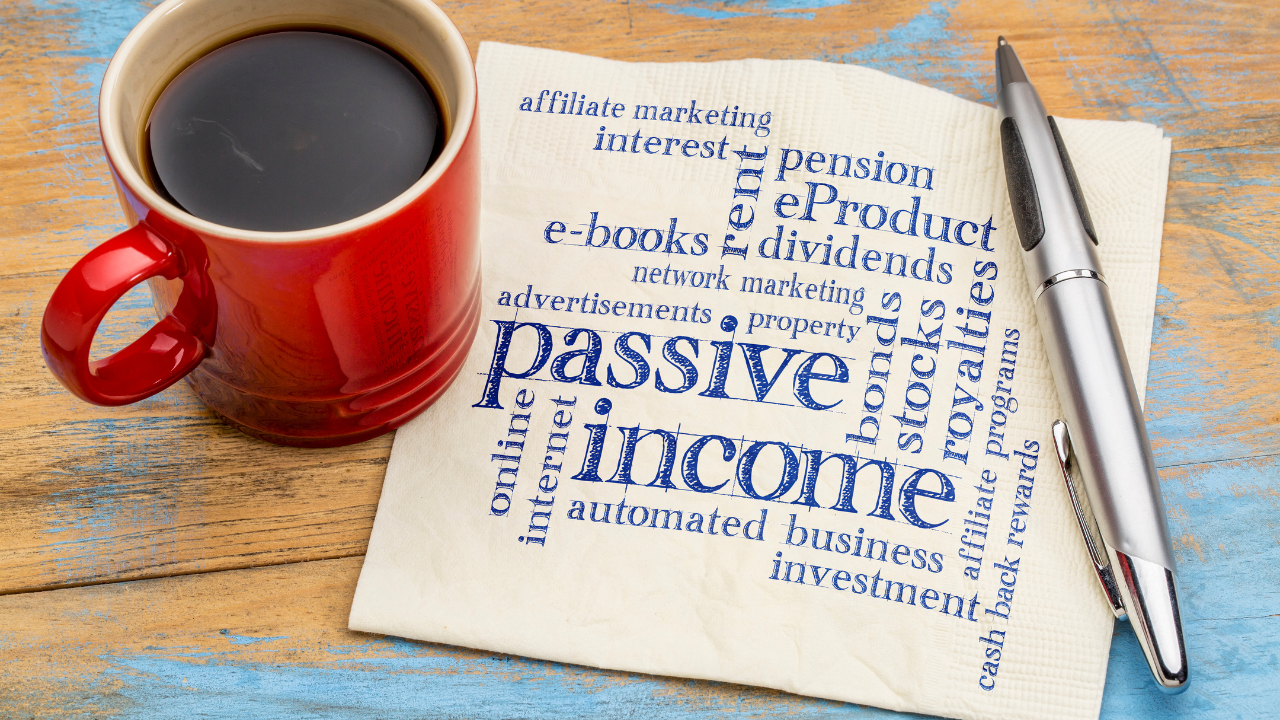

Build a Stable Future: Diversify Your Income as a Commercial Airline Pilot

We all like to take control!

That’s the feeling we get when we take hold of the yoke, or side stick, whether it’s a small single-engine plane, or a transport category aircraft and guiding it skyward, or manipulating the controls for a greased landing!

While we are in control of our flight path, many of us haven’t had the education or the checklist to take control of our financial flight path.

Even on a good day our income depends on so many factors out of our control: the weather; mechanical issues, ground stops, union negotiations, company policies and FARs (that’s Federal Aviation Regulations, for the non-aviation geeks reading!)

Then there is the once, or twice a year medical exam and scores of periodic training sessions, computer-based training and practice in the full-flight simulator.

Few other professions face our unique situation that often spans multiple time zones.

Few other professions face periodic layoffs and displacements – which either eliminate or decimate your ...

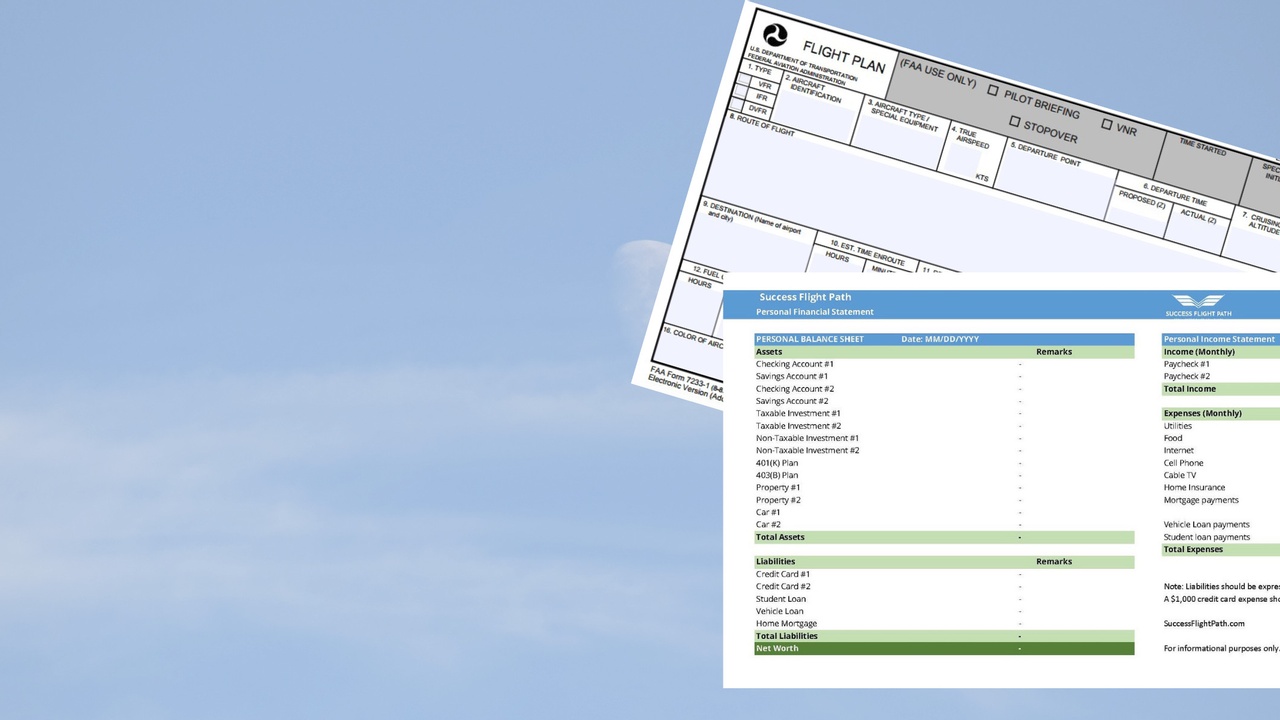

Planning for Airline Pilots: Where to Start

As a pilot, you have a unique set of financial planning considerations.

From managing the costs of flight training to saving for retirement, it's important to have a clear plan in place to ensure a secure financial future. Let's explore some of the key elements of financial planning for airline pilots.

Budgeting and Expense Management

The first step in financial planning is creating a budget and managing expenses. This means tracking your income and expenses to ensure that you are saving enough to meet your short- and long-term goals. Consider setting up a budgeting tool or working with a financial planner to help you stay on track.

Risk Management

As a pilot, you face unique risks, such as the possibility of disability or loss of life. To protect your finances in the event of an unexpected event, it's important to have adequate insurance coverage, including disability, life, and health insurance. Review your policies regularly to make sure they are still adequate and afford

...Knowing your business model gives direction

When you fly for a living - it's the best job in the world....until you get laid off, or displaced and have to juggle flying with the "real" world of paying bills.

In creating an additional source of income, it can be daunting to decide what to do, what to create, which opportunities to pursue.

Most businesses, and investments for that matter, can be tucked neatly into one of four business models.

Knowing which category your idea fits will provide guidance, to pinpoint your direction as to how to capture opportunity, minimize risks and avoid threats.

This is the part they don't teach you in basic flight school (which fits nicely in a B2C business model).

The four business models are:

1. B2C - business to consumer. This is the most common businesses module, where a business sells to a consumer. Basically anything you buy either in a store, or on line, say household supplies, light bulbs, clothing, entertainment (anything from Target or Home Depot!) fits in this category.

2. B2B - business to...

Secure your financial flight path with diversified income

Last week I was flying with a new hire First Officer and had a senior wide-body captain on the jumpseat.

After all the nice pleasantries and taking off, our conversation turned to the last year's turmoil - the cost Covid-19 had on the airline industry.

The new First Officer thought he had made it - landed a pilot job with a Legacy Carrier.

Both myself and the Senior Captain couldn't stress enough the importance of having a secondary source of income - just in case.

In the airline industry, it's never "just in case." It's not a matter of if, but a matter of when - when the industry takes a nose dive again.

It seems that aviation is hit with some sort of unpredictable and uncontrollable Category 5 financial hurricane ever eight to 10 years.

9/11

The 2008 recession

Covid-19 lock-downs

Several airlines didn't survive this round.

Hundreds of pilots received the dreaded news:

“Due to current unforeseen business circumstances beyond our control, the Company has made the ...

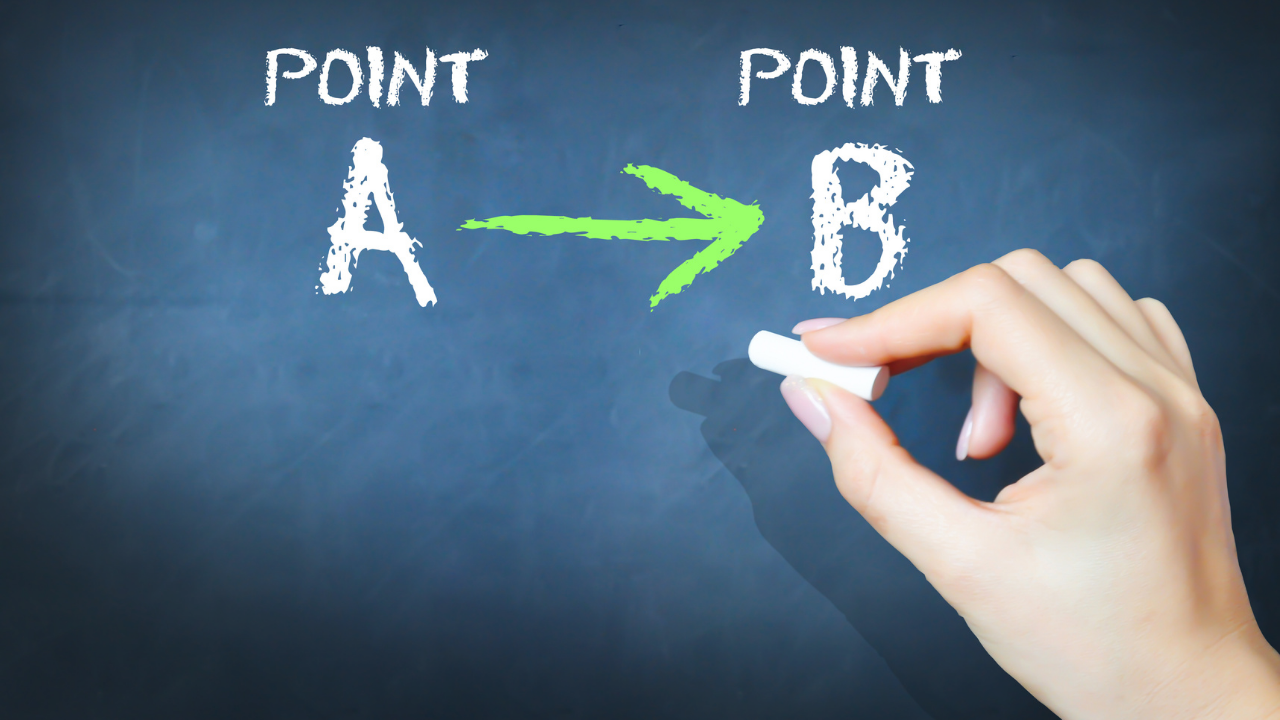

Flight Planning your Finances

When flight planning, do you begin with the departure point, or your destination?

How about planning for retirement, even if it's a few decades away?

Did you start when planning for retirement when you started flying, or will you begin right before you turn 65, when you're grounded by federal law?

Airline pilot unions do an amazing job with retirement seminars. But other than signing up for the company 401k or other retirement programs, there is little to no education on what to do with your money.

Do you roll the dice with a pre-selected investment strategy? Do you manage the account your self or get help?

One area to start is to work the numbers backwards. Where do you want to be at the end of your flying career? Start a Point B. You already know where your starting point.

Do you want to retire with $3,000 a month income?

$10,000 a month?

$20,000 a month?

Is it all going to come from your 401k, or defined benefits plan? Or will a portion of that co...

Hitting financial wake turbulence

Whew, did we hit financial wake turbulence last year!

Many pilots slammed into major wake turbulence in 2020 because they didn’t have a financial flight plan!

As pilots, we train for the "unexpected" so that when something goes wrong in our aircraft, we are ready and prepared. Flight instructors have hours of instruction on how to get out of wake turbulence, but no one teaches us how to recover from hitting financial wake turbulence.

In fact, in most cases, professional pilots get little to no financial education before taking the controls of their aircraft.

It’s imperative that we prepare for the unexpected in the cockpit and in our bank accounts, especially when it comes to financial wealth building. Last year’s downturn was caused by factors well beyond our control....like furloughs and layoffs.

But the devastation in the airline industry and our national economy jolted most households, while others took it all in stride.

What was the difference? Whether or n...

Stressed about money? You're not alone.

Is the state of your finances stressing you out?

You're not alone.

A recent survey showed that finances are the #1 cause of stress.

Politics, work and family issues followed suit.

But there are a few strategies you can use to minimize financial stress. Here they are:

✈ Get clear on your financial situation - How much do you make? How much do you owe?

✈ Get Financial Goals - think about how money stresses you - Are you in debt? Are you living paycheck to paycheck?

✈ Set priorities about paying off debt - How much is the debt, plus the interest on that debt costing you financially and emotionally?

![]()

✈ Create a budget - or a guideline for your money! Make it easy on yourself but don't forget to set aside a bit of money to enjoy.

✈ Check your accounts on a regular basis. This allows you to see if your cash flow doesn't align with you goals, or if there has been fraudulent activity.

✈ Don't be hard on yourself. Every once in a while you are going to spend more than you wanted. Just realize that a p...

Drop the Debt Burden

- Set an achievable goal

- Make a budget, including debt repayment

- Use an app – make it easy

- Improve your credit score

- Try avalanche method of debt repayment

- Try the snowball method of debt repayment

- Adjust savings goals

- Adjust, or establish investment contributions

- Consider balance transfers to credit cards with lower interest rates

- Negotiate credit card rates

- Check your credit report

- Talk to a debt counselor, if applicable

- Ask for debt reduction

There is "good" debt - such as mortgage debt the produces income, but most Americans carry consumer debt that not on

...